June inflation report came as a surprise to investors, however, there seems to be no major shift in Fed expectations after the release. The intraday market reaction after the release of the report was quite emotional: USD soared up, long-dated Treasuries fell in price and US stock indexes slipped. By Wednesday, those movements ran out of steam: 10Yr Treasury bond yield retreats, futures for US indices trade in green while USD completely unwound post-report gain:

Should we expect Powell to address persistent inflation in his speech today and hint at the possibility of an even earlier withdrawal of stimulus? I think not, and here's why.

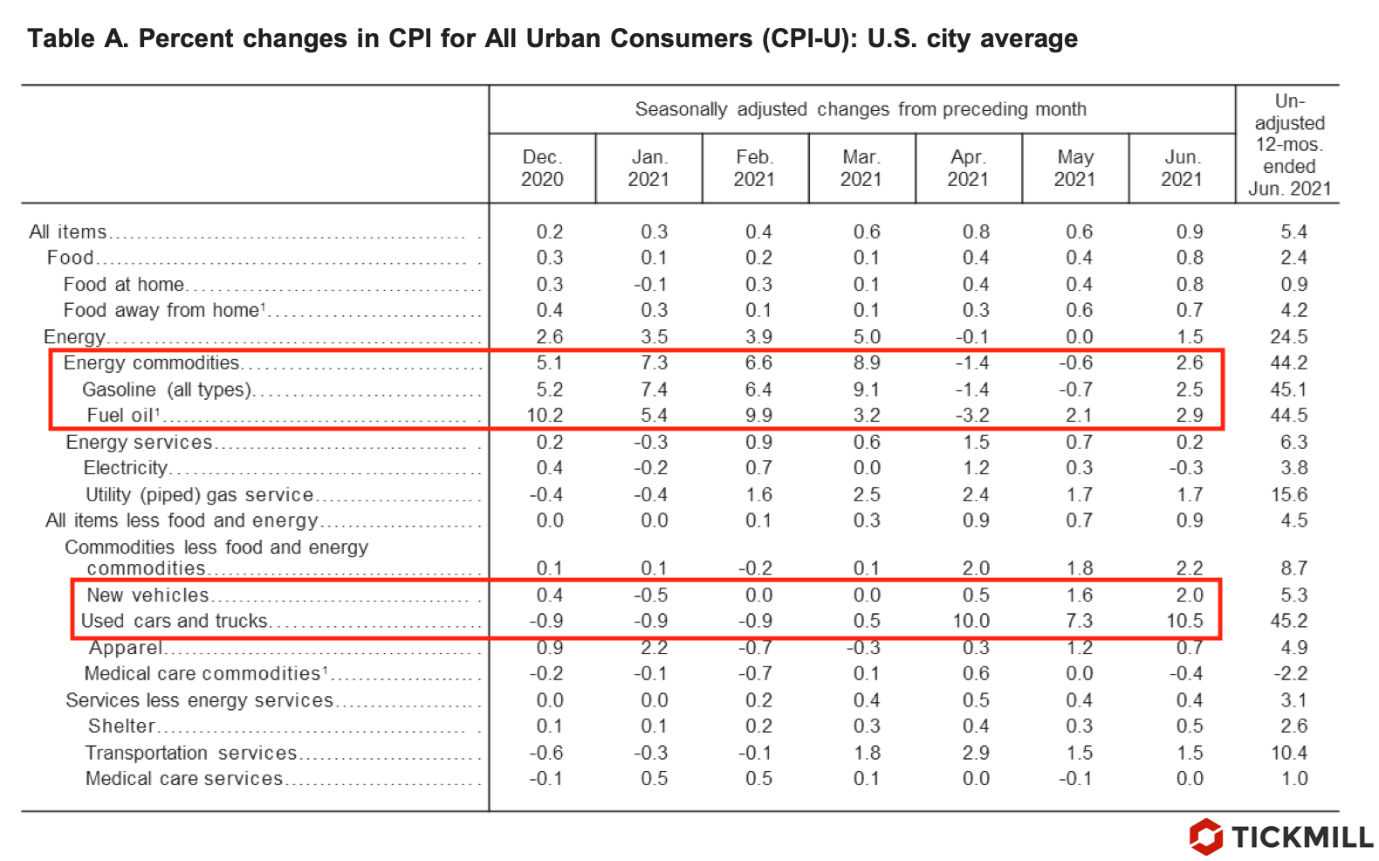

Trying to decipher whether high US inflation is temporary or not, i.e. whether or not the Fed should try to adjust the policy or rhetoric in response to its behavior, it might be useful to break it down into key consumption categories and consider contribution of each separately, since there are temporary and permanent drivers of inflation. Consider contribution of the main components in June in the table below:

I marked in red the positions that made the main contribution to inflation. It can be seen that the monthly inflation rate for used cars was 10.5%, breaking this year's record. At the same time, the percentage contribution of this component to the CPI reading was about one third.

Fuel price inflation also made significant contribution. On a monthly basis, gasoline prices rose 2.5%.

Otherwise, it can be seen that the numbers are very, very modest. For example, the rental rate for primary residence increased by an average of 0.23% on a monthly basis.

The increase in the price of used cars and fuel can be confidently attributed to temporary drivers, since the demand for them is caused by stimulated consumer demand due to fiscal support measures, seasonal factors as well as world oil prices. Therefore, it would be strange to believe that the Fed will change its opinion on inflation after this report. Markets seem to have also digested the information and the consensus on temporal nature of recent high inflation remains dominant, which is evident, in particular, from the absence of investor flight from long-dated bonds and weak USD performance today.

Post a Comment